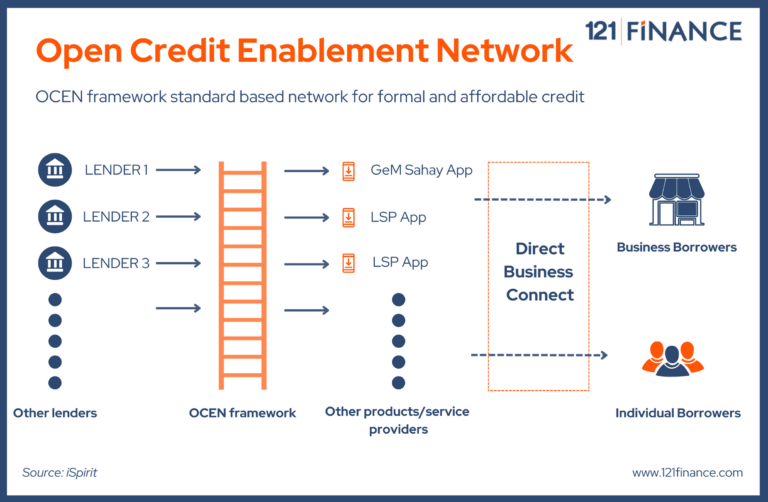

› Access to Affordable Credit: One of the significant challenges faced by MSMEs is obtaining affordable credit from traditional financial institutions like banks. OCEN aims to create a decentralized credit ecosystem where various lenders can participate and offer credit to MSMEs at competitive interest rates, thereby increasing their access to much-needed funds for business growth and expansion.

› Increased Financial Inclusion: Many MSMEs lack formal credit histories, making it difficult for them to qualify for loans from traditional banks. With OCEN, alternative data sources can be utilized, such as digital transaction records, to assess creditworthiness.

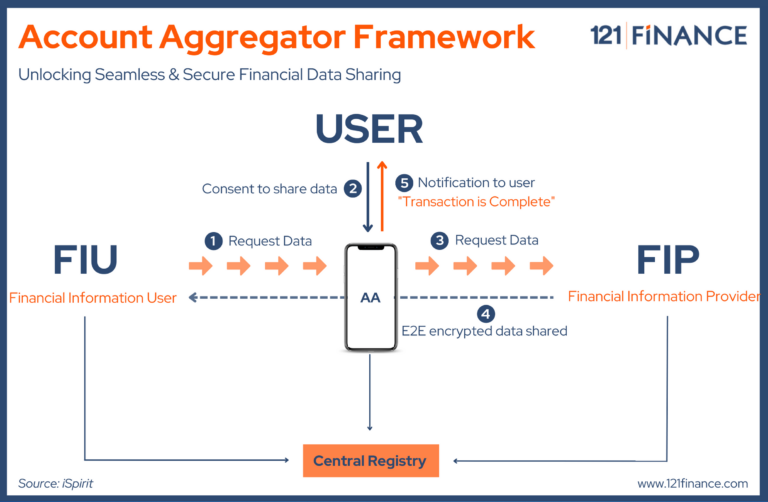

› Transparency and Security: OCEN operates on distributed ledger technology (blockchain), which ensures transparency and security in transactions. Every participant in the network can view the data and verify the authenticity of transactions, minimizing the risk of fraud and enhancing trust among lenders and borrowers.

› Reduction of Intermediaries: In traditional credit ecosystems, there are several intermediaries involved, leading to higher transaction costs for borrowers and lenders. OCEN aims to eliminate or reduce the number of intermediaries, which can result in cost savings and more efficient credit allocation.

› Flexibility in Loan Products: With multiple lenders participating in the OCEN network, MSMEs can access a diverse range of loan products tailored to their specific needs.

› Quick and Seamless Loan Approval: Traditional loan approval processes can be time-consuming and tedious. OCEN’s digital platform enables streamlined loan application, verification, and approval processes, leading to quicker access to funds for MSMEs.

› Data Privacy and Control: While using alternative data sources for credit assessment, OCEN emphasizes data privacy and empowers MSMEs to have control over their data. It allows businesses to choose what information to share with lenders, enhancing data security and minimizing the risk of data misuse.

› Improved Credit Rating and Reputation: Timely repayment of loans through the OCEN network can contribute to building a positive credit history for MSMEs. This can enhance their credit rating and reputation, making it easier for them to access credit in the future.