121 Digest – Why Businesses Still Struggle to Access Credit

January 2026 Issue: 25 Why Businesses Still Struggle to Access Credit? Quote of the Month "Opportunities come infrequently. When it rains gold, put out the bucket, not the thimble" Did you Know?

Best Collateral-Free Financing Options for Small Businesses in India

Collateral Free Business Financing

Factoring vs Traditional Business Loans

Factoring Finance vs Traditional Loans Which is Better for Your Business? Factoring Finance isn’t a loan, it’s a smarter way to get paid faster and keep your business growth intact.

The Economic Power of Culture: How Global Cultural Habits Influence GDP Growth

The Economic Power of Culture How Global Cultural Habits Influence GDP Growth India being a country of festivals, starting the year with Pongal/Makar Sankranti and ending it with Christmas, it

Revenue Based Financing vs Factoring Finance

Revenue Based Financing vs Factoring Finance Which Flexible Funding Solution is Right for Your Business? Today, businesses are constantly looking for alternate funding options that can benefit them. They want

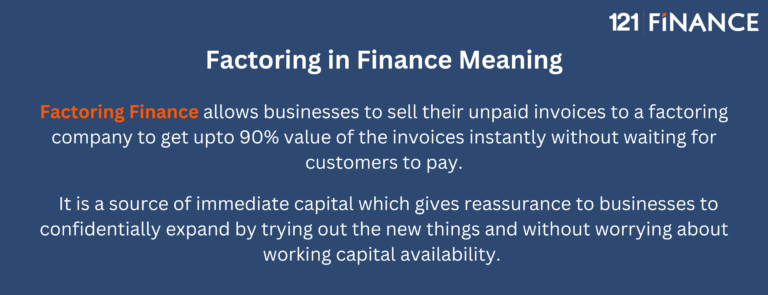

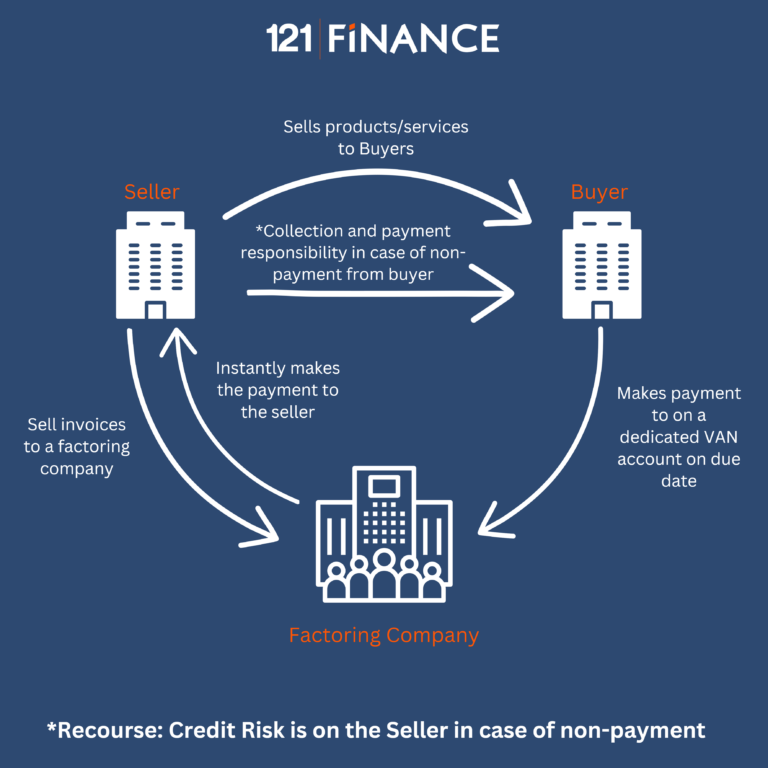

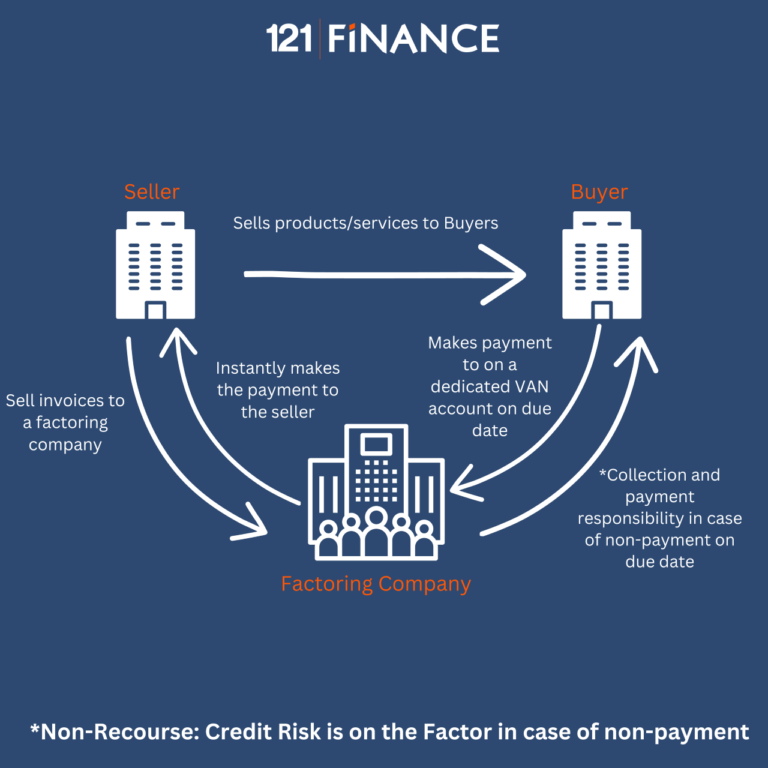

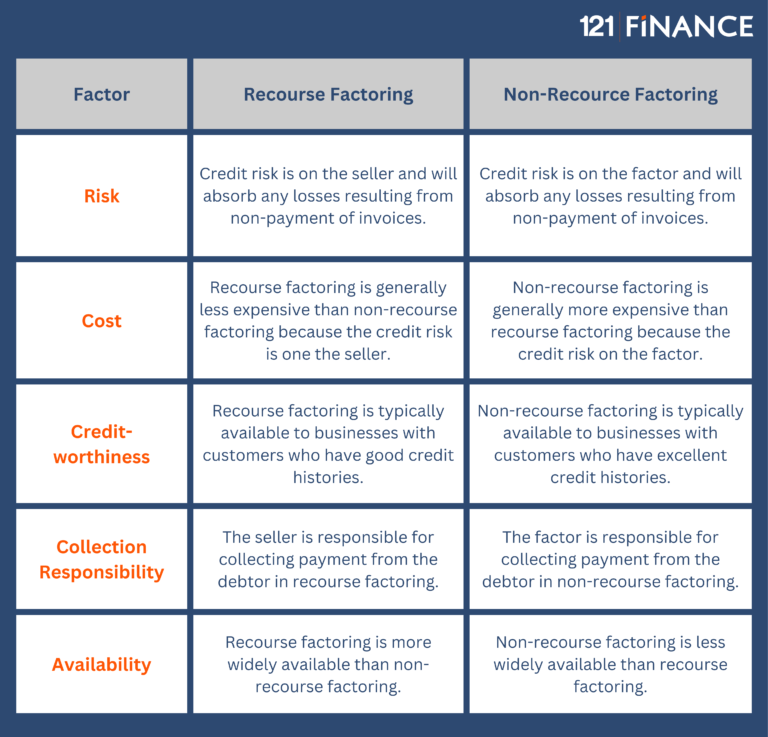

Introduction to Debtor Finance

Introduction to Debtor Finance